2021 RETAIL SURVEY: A YEAR OF UNCERTAINTY

Menswear merchants remain determined to reinvent the business but cash flow issues, unreliable deliveries, and erratic consumer shopping patterns are proving problematic. Even so, business is picking up!

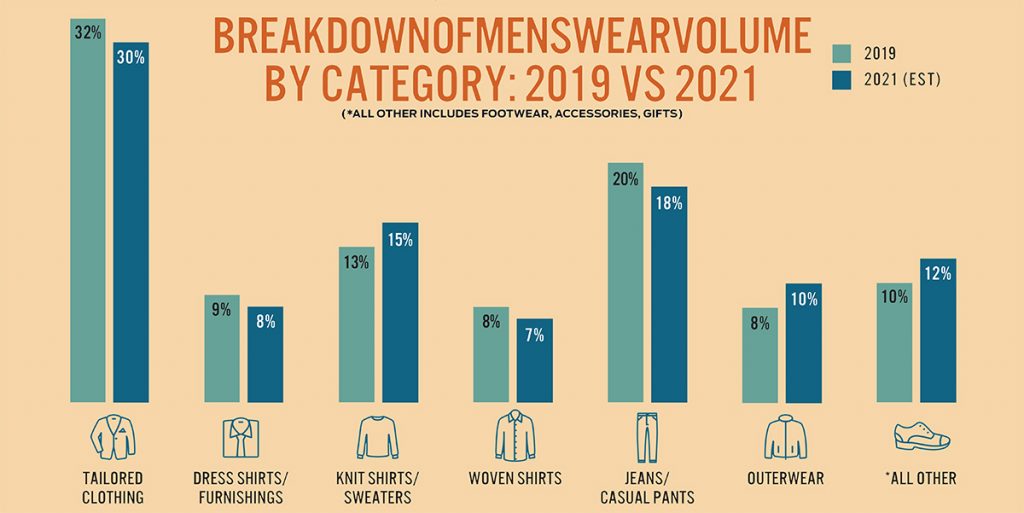

As retailing in the U.S. begins its post-pandemic rebound, candid menswear merchants admit a good degree of uncertainty. Most are doing some suit business since weddings are back on the calendar, but does this portend an actual return to tailored or just a temporary shot in the arm? Many are selling activewear and expect joggers and comfort knits to play a bigger role into fall; others believe guys are tired of looking sloppy and see “elevated sportswear” as the way to go.

While many retailers say they’ve gotten beyond the cash-flow issues, others admit it’s still a problem, so they’re scrutinizing every buy. Most have cut back on expenses and will try to keep costs low while others aren’t so sure (“my landlord won’t let me…”). Several who reduced staffing are now struggling to find strong sales associates. Many merchants have downsized or else are looking for smaller spaces; almost all are more closely tracking inventory and are newly focused on in-stock programs. Some who cut back on advertising are now hoping to reinstate lookbooks and magazines; others wonder if they can afford to. Almost all say they want to develop their online business but very few have actually made the investment. Bottom line: virtually everyone admits some degree of post-pandemic indecision. Or as one merchant put it when asked how he’s planning spring ‘22, “I really don’t have a clue.”

But one thing is certain: with so much menswear now transacted online, a backlash seems inevitable. “Shop Local” “Support Community” have become universal mantras; independent retailers who are reestablishing strong bonds with their customers (and neighboring small businesses) are reaping the rewards. Old fashioned phone calls inviting customers into the store (to view new product, to enjoy a coffee or a beer, to simply hang out) are proving every bit as effective as email and social media. Facebook videos by store owners describing new fashion receipts are driving in-store traffic. Collaborations with non-competing businesses (buy a new Italian sportcoat and wear it to the local steakhouse for a free bottle of wine with dinner) have worked well for some creative merchants. In-store events, even trunk shows, are also working again has customers long to congregate, socialize, and drink wine!

RETAILERS ON BUSINESS

*Business Year-to-Date: 35 percent are up (almost at, or slightly ahead of, 2019 levels), 50 percent are down (20-60 percent range), 15 percent say business varies tremendously day-to-day. (Many merchants admit they did not buy aggressively enough and were hurt by poor deliveries.)

*Fall ’21 plan vs. 2020: up average 20 percent over fall 2020.

*Pent-up consumer demand? 40 percent say it’s exaggerated, 30 percent say it’s real, 30 percent don’t know.

*Spring/Summer ’21 Best Sellers: Soft Jackets (chore jackets, safari styles), luxury polos, five-pocket pants in luxury fabrics, vintage-looking knits, denim, MTM clothing, activewear, shorts, all things new, suits (in some stores).

*Spring/Summer ’21 Top Brands: Ermenegildo Zegna, Canali, Isaia, Brunello Cucinelli, Eleventy, Baldassari, Etro, Kiton, On Running shoes, Peter Millar, Faherty, Johnnie-O, Rodd & Gunn, Orlebar Brown, Brax, AG, 34 Heritage, J Brand, Jacob Cohen, PT Torino, MAC, Eton, Stenstrom, Masons, Meyer, Patrick Assaraf, Vuori, Greyson, Gran Sasso, Paul & Shark, and Vastrm.

*Worst Sellers: Suits, ties, loungewear, spring sweaters, dress shoes, streetwear, fashion-forward designer product, dress pants, over-the-calf socks.

*Projected Fall ’21 Best Sellers: Outerwear, luxury knitwear, soft sportcoats, activewear, cashmere, customization.

*Projected Spring ’22 Best Sellers: Faherty, Johnnie-O, Peter Millar. According to numerous luxury retailers, “These brands are HOT this season but generating too high a percentage of the business, bringing down our AUR…. Still, how can we cut back on our fastest turning product?”

*What’s Needed To Jumpstart Sales: A new work uniform; jersey suits; hooded blazers; nice woven shirts, especially Italian (hard to find with so much movement to knits), pleated trousers; soft DB blazers; better messaging (more ads encouraging guys to elevate their look), higher pricepoints, higher margins, better deliveries, shipments timed to consumer shopping patterns, more wear-now fashion, more private label.

KEY CHANGES MERCHANTS ARE MAKING

From a Minneapolis store: “We’ve added women’s and plan to grow it. Will grow tailored clothing as it seems to be coming back. We’re becoming more liquid and chasing more business. We’re supporting a core assortment and reassessing it more frequently, but also introducing new brands on a more regular basis. We’re buying more wear-now fashion.”

From a Houston store: “We’re planning a major capital spend in 2022—either a remodel or new location to create a better in-store experience. We’re looking for more contemporary lines, more denim and heritage looks. We’re hoping to add some non-apparel items; we dropped our women’s business last year.”

From a New Orleans store: “We’re staying in closer touch with our customers; we find this more important than increasing sales right now. Also, we’ve made some salary adjustments, cutting hours on some full-time sellers. Fortunately, they understand that tourism is down and it could take until 2022-23 until it’s back.”

From a Charlotte store: “We’re bring in private label MTM at accessible prices to attract younger guys. We’re pushing luxury sportswear. We’re paying attention to every nuance so we can turn on a dime.”

From a Chicago store: “We cut expenses 50 percent but we’re unlikely to stay at this level. We’ve expanded the categories we introduced during Covid, especially golf which I never really wanted. We’re paying more attention to improving turn on in-stock inventory. But we don’t want to get too basic: competing with A-doors of Neiman Marcus, Nordstrom, and Saks Fifth Avenue, our customers expect fashion. We’re displaying more in-store vignettes of different lifestyles.”

From retail consultant Steve Pruitt: “Rather than making changes now, we need to stay on top of the changes we’ve already made by focusing month to month on our receipt plans and the timing of deliveries.”

From retail consultant Danny Paul: “Most stores got rid of staff that they didn’t need in the first place and are now operating with lower rent. The goal now is to invest in technology and social media. Retailers are always looking for new brands but they might want to consider fewer of them going forward. A good formula for a profitable business: fewer vendors, lower rent, less staff, less inventory, higher turn.”

TIMING IS EVERYTHING

Numerous retailers insist that deliveries are still a big problem, and are likely to get worse. “Vendors don’t seem to care and don’t feel accountable for bad deliveries,” writes one. “I can already hear the excuses for fall (pretty cynical of me, I realize) which is why I’m spending more time than usual in NYC showrooms to ensure the goods will at least be in the country so we can control the flow.” Another retailer wrote about the number of shipping errors this year: duplicates, incorrect product, additional sizes, all of which were sent back. “When delivery extends beyond the window we request, we ask for a discount or decline the order after the cut-off date.” A different retailer notes that customers are shopping in season so vendors would do well to shift the timing of production to reflect how customers shop. Notes retail consultant Danny Paul, “Vendors need to understand that retailers can no longer place orders six to 10 months in advance. They will need to respond in less time.”

THE POWER OF NEW

Most retailers agree that fresh new product from new brands would add excitement to the selling floor and hopefully attract new customers but that it’s easier said than done. “I’d been planning to bring in new product but it’s tough when I haven’t been in showrooms. Virtual shopping didn’t work for me.” “I’m going to reevaluate my vendors more frequently,” writes another. “I just dropped a clothing collection that I’d been using for years because the product was too boxy, not at all sexy. I replaced it with a more modern fit that I think my customers will prefer.”

“We’re still trying to figure out what fashion means to men post-pandemic,” admits another. “Most of the newness seems to be in outerwear and knitwear as opposed to clothing or sportswear. We’re bringing in many new brands in 2021 but we’ll probably decelerate the pace next year.”

WHY CAN’T WE JUST GET ALONG?

Surveyed retailers were divided in their feelings about retailer-vendor partnerships going forward. Almost all have accepted the fact that most of their vendors now sell direct, which some say is no big deal unless they blatantly discount. “I don’t get why things have to be so adversarial,” writes one merchant. “The hot lines are raising their minimums or else they’re ‘reimagining their retail distribution.’ There are suddenly rules for everything. Whatever happened to business on a handshake?” Another merchant sees it differently, “Vendors are working hard to move through their shipping and production problems and it can’t be easy to suddenly speed up their production time. That said, we need to work together to focus on the big ideas. As a retailer, I could really use more concrete conceptual direction.”